Carbon credits are not a typical commodity. Although crediting programs provide some assurance, purchasing higher-quality carbon credits is not as simple as buying any “certified” credit issued by a crediting program. Some credit buyers can invest the time and resources to research and discover good projects and procure higher-quality credits. For many (if not most) buyers, that approach is not realistic. This section describes – and assesses the pros and cons of – some strategies for steering clear of lower-quality carbon credits.

Most reliable methods

The following approaches for avoiding lower-quality carbon credits are the most effective. These approaches rely upon quality assessment by actors with significant technical expertise. Still, these methods are not a guarantee against lower-quality and should be pursued carefully and with attention to specific details.

- Buying credits from projects rated highly by independent rating service

- Vetting crediting projects directly

Buying credits from projects rated highly by independent rating services

Carbon credit rating services that rate the quality of individual projects are relatively new to the voluntary carbon market. In line with this guide’s presentation of how to think about carbon credit quality (see What Makes High-Quality Carbon Credits), existing services typically provide nuanced ratings that distinguish relative quality on a sliding scale, often across different criteria and quality dimensions (e.g., additionality, quantification, permanence, exclusive claims, and avoidance of social and environmental harms).

In practice these services interrogate projects in line with (some version of) the recommendations found in vetting carbon crediting projects directly. Some rating services offer bespoke ratings for individual clients.1 Others may team up with specific platforms to make their ratings available, such as the Salesforce Net Zero Marketplace or Allied Offsets which host ratings from three credit rating companies (for some listed projects). In 2023, Carbon Market Watch published a review of existing services and how they conduct their ratings. However, (when this page was published in 2024) all such services were operated as for-profit companies that typically do not divulge the details of their rating methods, nor do they typically make their ratings publicly available.

Pros: Relying on individual project ratings, conducted by a rigorous and reliable rating service, is probably the strongest way to avoid lower-quality carbon credits (short of conducting one’s own project-level due diligence). Such ratings can help buyers avoid lower-quality projects that may slip through the standards and vetting processes of carbon crediting programs, and provide a more nuanced approach to assessing carbon credit quality than simply looking at methodology-level reviews. Looking at project-level ratings is perhaps the only reliable way to discover individual higher-quality projects (see What Makes High-Quality Carbon Credits) in “higher risk” categories.

Cons: Most rating services are operated by for-profit companies who treat their procedures as confidential intellectual property. Buyers therefore need to pay for these services, which can add to cost, and in some cases the rating methods may still not be transparent. In addition, as the Carbon Market Watch report referenced above makes clear, different services sometimes attach markedly different scores to the same projects. Some discretion may therefore still be warranted in relying on any particular service provider.

Vetting crediting projects directly

Buyers can ask basic questions about crediting projects that may help screen out lower-quality options. In most cases, project developers and carbon credit owners should be forthcoming with answers to such questions (if they are not, it is a red flag). The level of effort required to investigate a crediting project can vary, depending on a buyer’s resources and the type of project involved. One option is to engage the services of consultants or trusted retailers to examine projects. It is often a good idea to work with someone who has a detailed understanding of the sectors or project types being considered, which in some cases could involve enlisting multiple experts.

Pros: For buyers with time, resources, and expertise, vetting crediting projects can provide deep and direct insight into their merits and relative quality. As with using carbon credit rating services, this approach can help to avoid lower-quality projects, and to discover individual higher-quality projects within “higher risk” categories. It may be the only way to discover such projects if they have not been rated by a rating service.

Cons: Vetting projects directly requires time, expertise, and resources, and may not be feasible for many buyers. It may also be an inefficient way to discover higher-quality credits for buyers interested primarily in “common” project types already assessed by rating services.

For more sophisticated buyers with the resources to perform this due diligence, see the guidance to conduct crediting project “due diligence” for each quality criteria below. There is also a sample case study provided.

Read more about What Makes High-Quality Carbon Credits.

More reliable methods

The following approaches for avoiding lower-quality carbon credits can be more effective. However, they are not a guarantee against lower-quality and should still be pursued carefully and with attention to specific details.

- Sticking to lower risk project types

- Buying credits from trusted exchanges or retailers

- Buying credits from projects certified against independently assessed, higher-quality methodologies

Sticking to lower risk project types

Although many kinds of projects can avoid emissions or enhance removals, some types of projects have a harder time meeting essential quality criteria than others. Industrial gas destruction projects typically have clear additionality, for example: as long as they are not required by law, there are few if any reasons to undertake them aside from generating carbon credits.2 For many renewable energy projects, on the other hand, careful scrutiny is required to determine whether the prospect of carbon credit sales played a decisive role in their implementation (and even with such scrutiny, it can be hard to be certain – as they are often on the margin of viability with energy sales revenue alone).

Perhaps the easiest way to reduce the risk of buying lower-quality carbon credits is to restrict purchases to credits that come from lower-risk project types. The table below provides an overview of the relative quality risks associated with common types of carbon crediting projects.

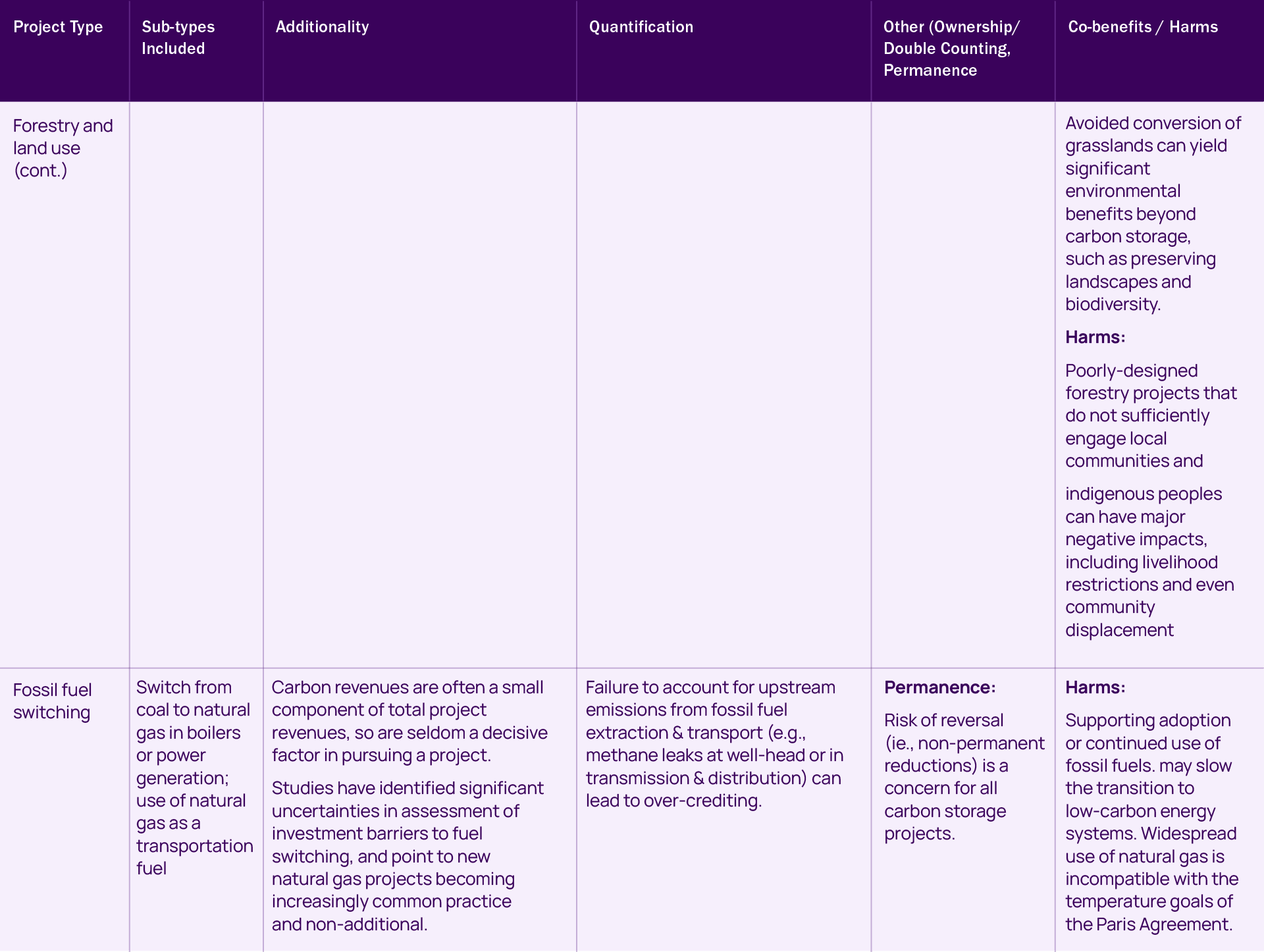

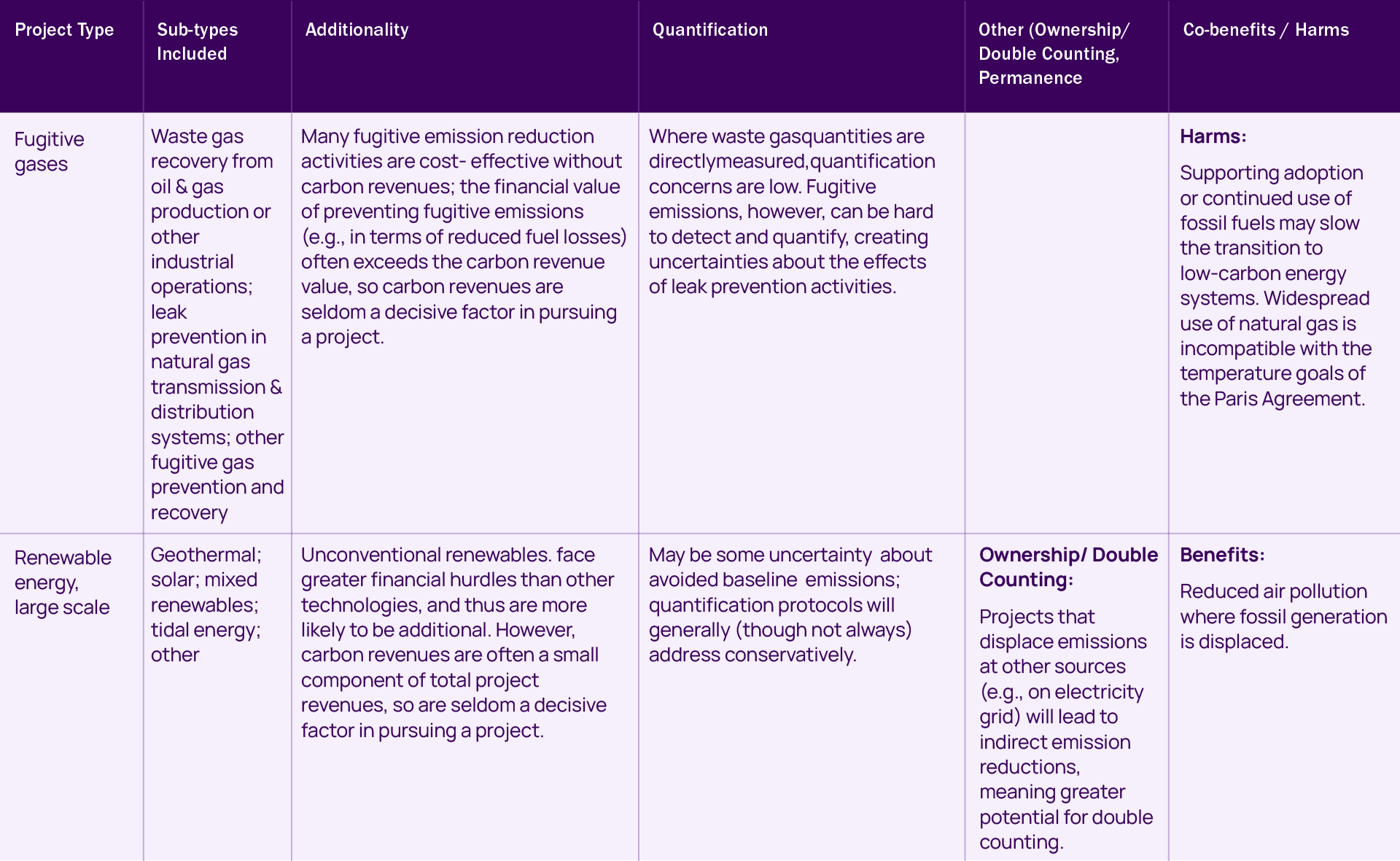

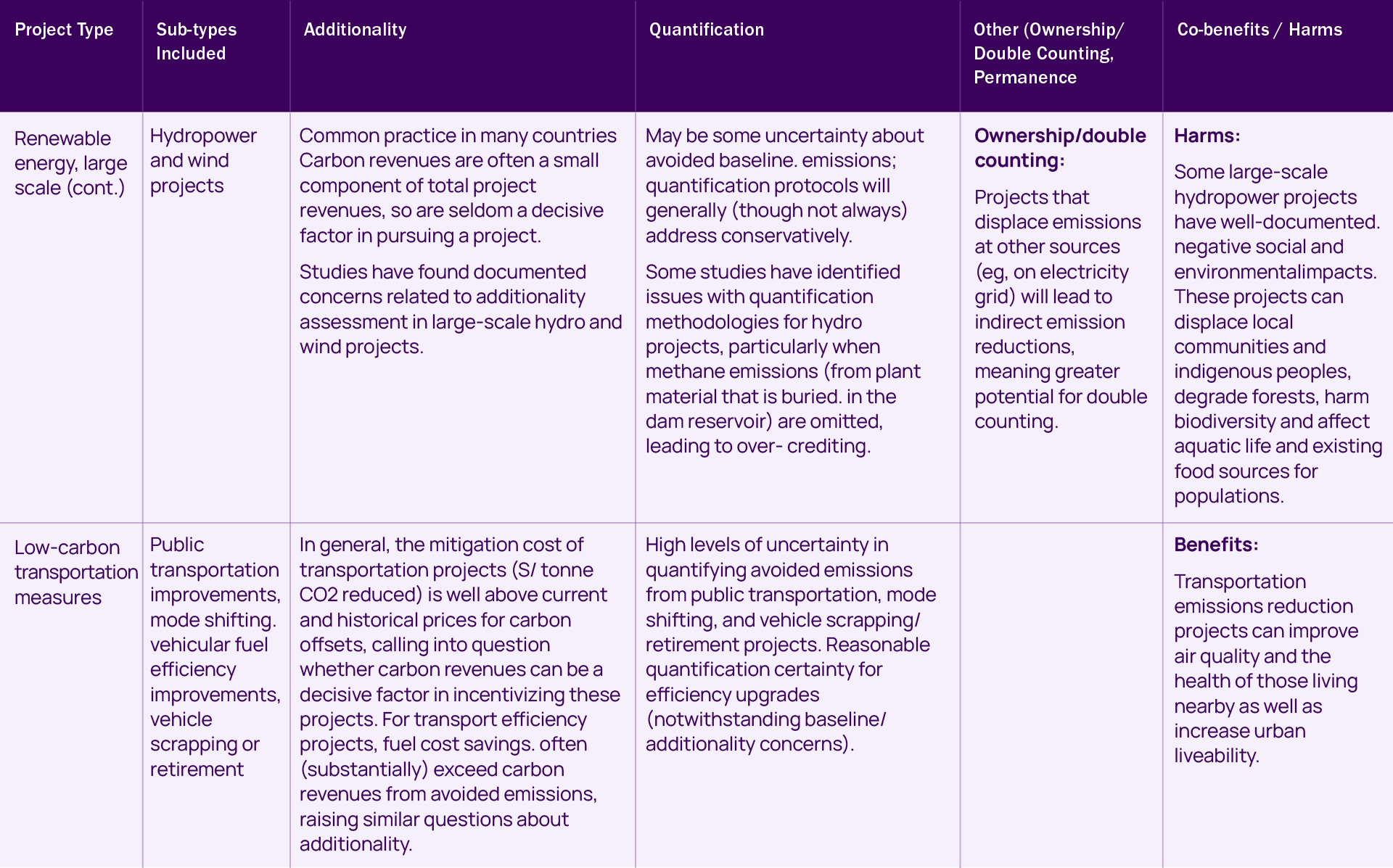

There are two potential drawbacks to this approach. First, as the table below indicates, there are only a handful of project types that have low environmental integrity risks as a class. Second, the kinds of projects that can most easily meet environmental integrity requirements tend to be projects that offer the least in terms of environmental and social co-benefits – and vice versa. Often, a buyer must choose between a project type with lower quality risks and one with greater co-benefits. A project that avoids N2O emissions at a nitric acid plant, for example, will generally be highly additional, easy to quantify, will pose no ownership or permanence concerns, and will not cause social or environmental harms – but it will do little to enhance people’s livelihoods or otherwise improve the environment. An agroforestry project that sequesters carbon in trees across many small farms, on the other hand, may yield a multitude of local benefits – but its GHG impact will be harder to quantify, and the carbon stored in trees may not be permanent. These kinds of trade-offs can be observed in the tables below that specify Lower-, Medium-, and Higher-Risk Project types that are linked below, which also identify the project types that offer the greatest potential for social and environmental co-benefits.

Pros: Sticking to project types that have a lower risk for quality deficits (e.g., because they typically are additional, are easier to quantify, and do not pose permanence, double counting, or social and environmental harm concerns) can be a relatively easy way to avoid low-quality carbon credits.

Cons: Lower risk is not the same thing as a guarantee of quality. The standards and methodologies used to certify projects may still be important. Furthermore, limiting purchases to lower risk project categories may exclude many valuable mitigation activities, including those with social and environmental co-benefits.

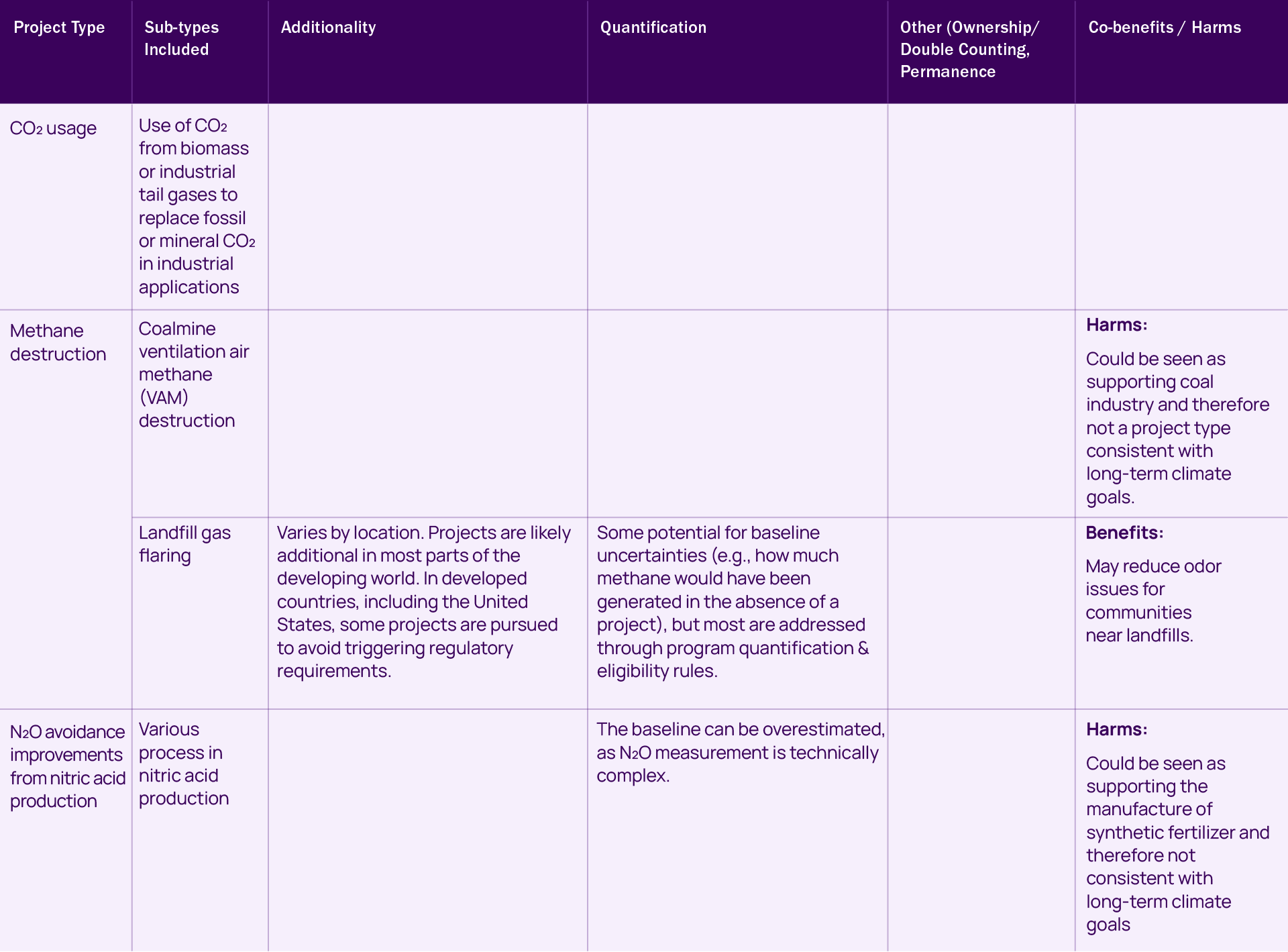

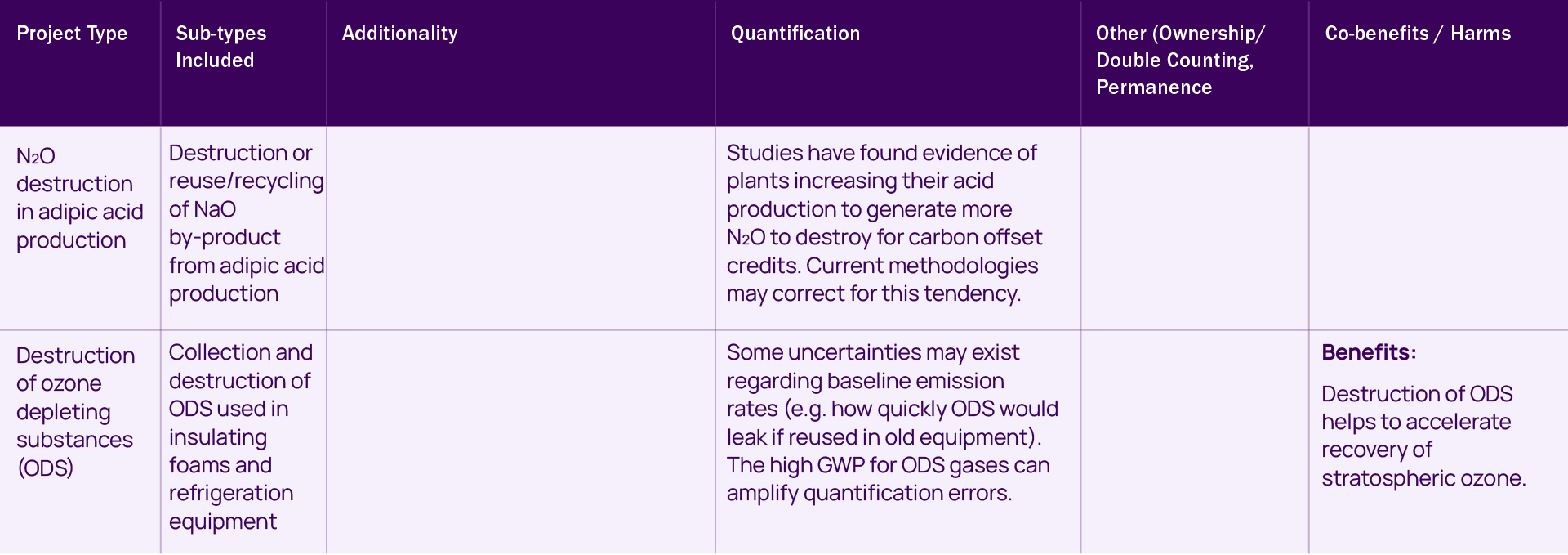

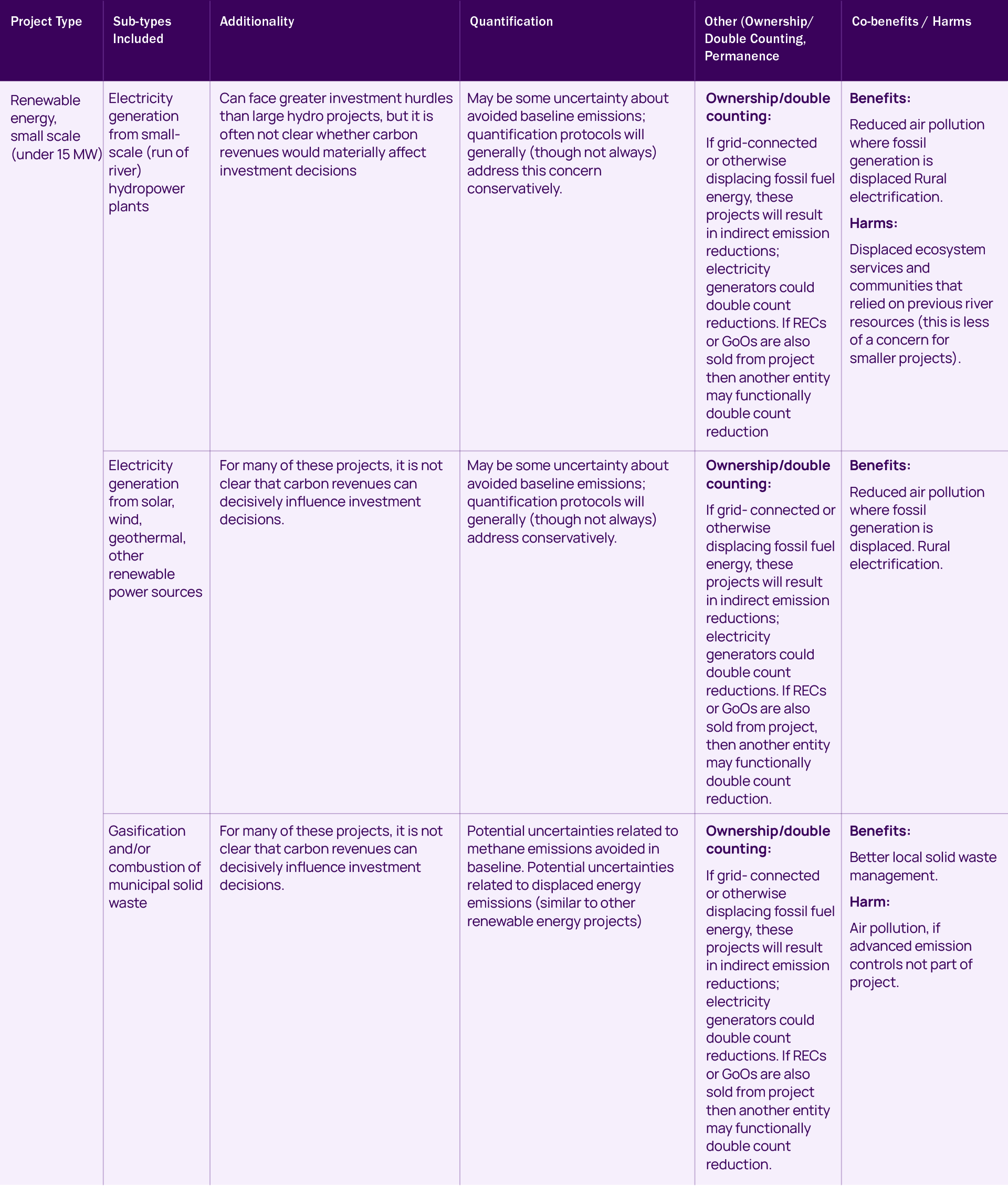

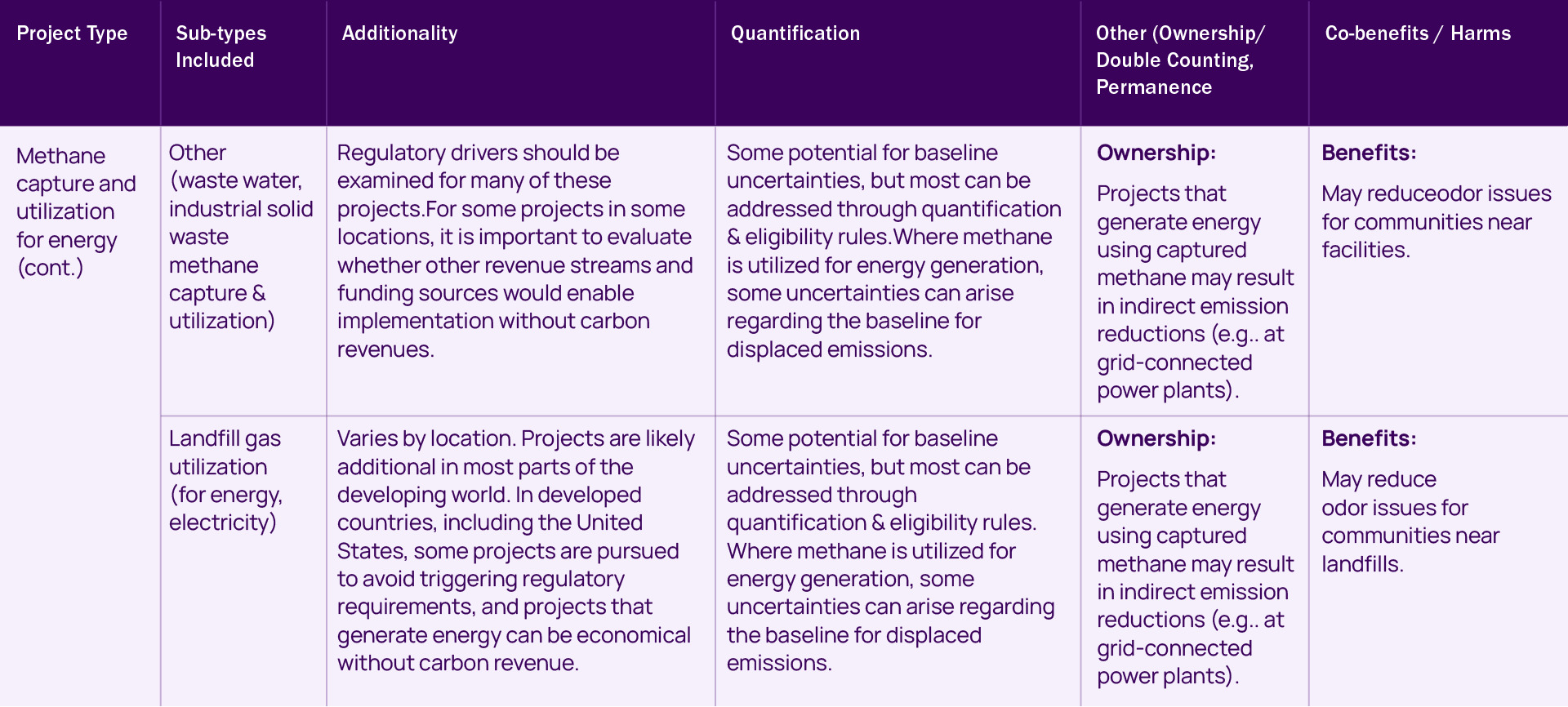

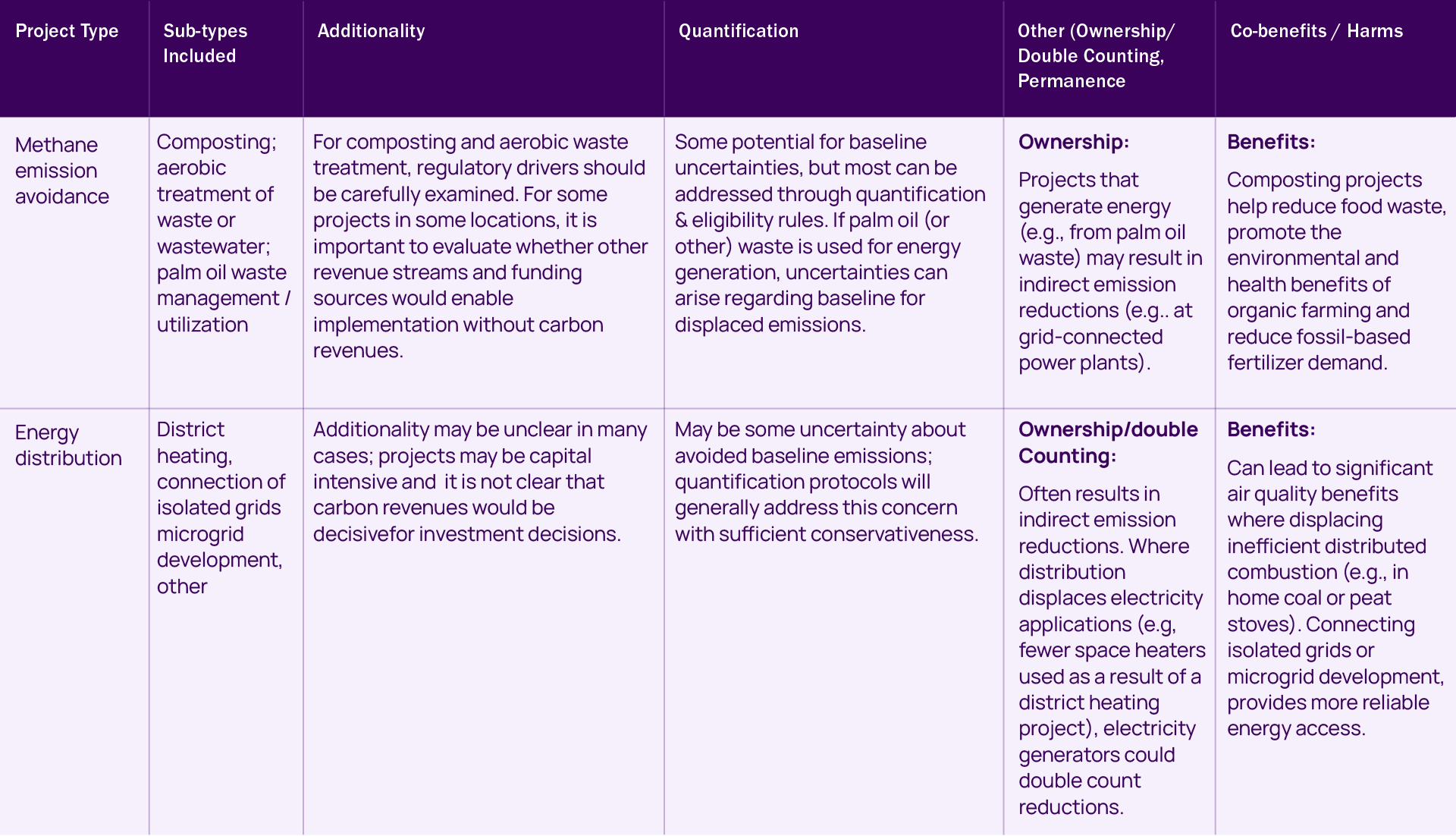

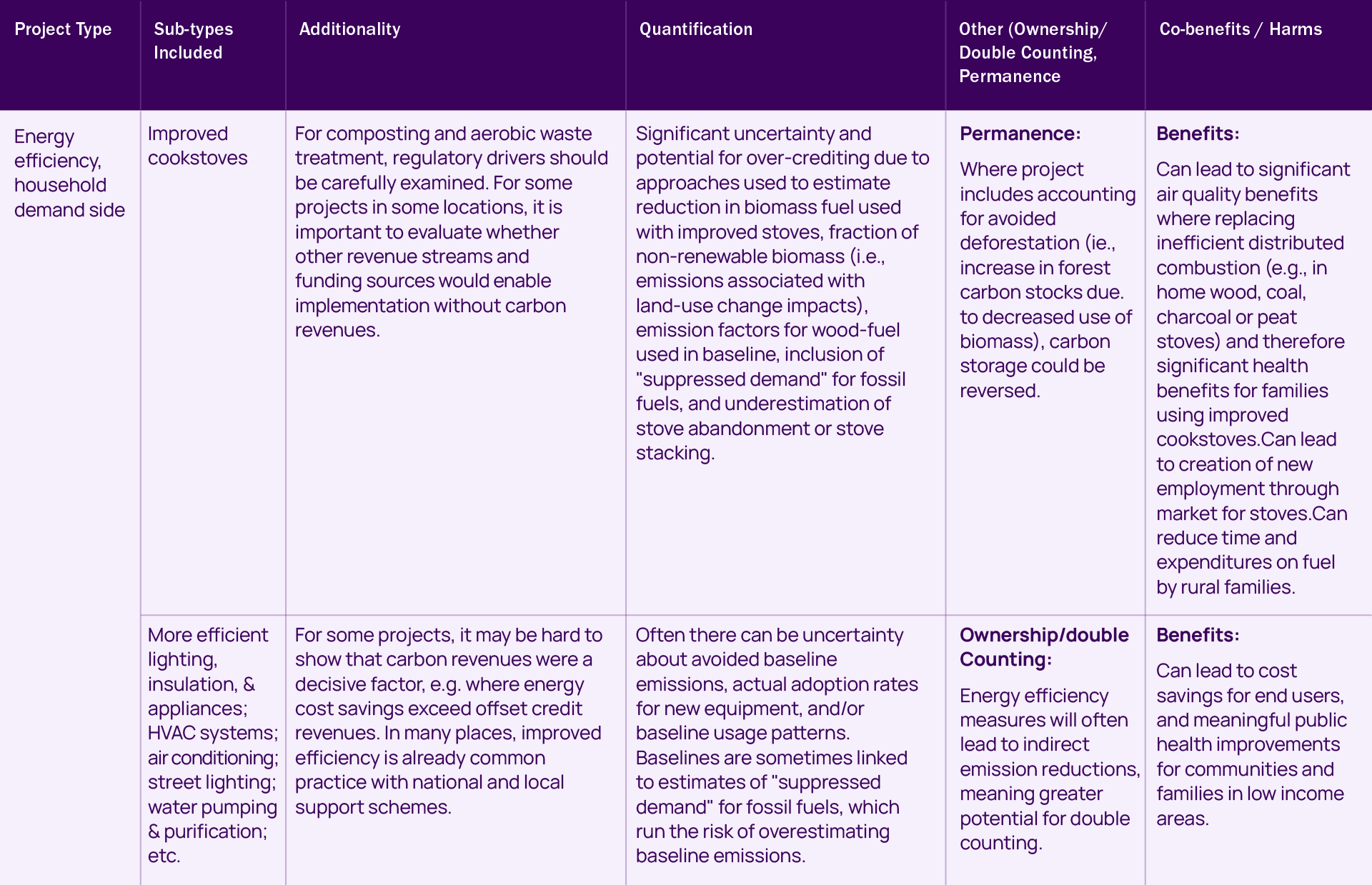

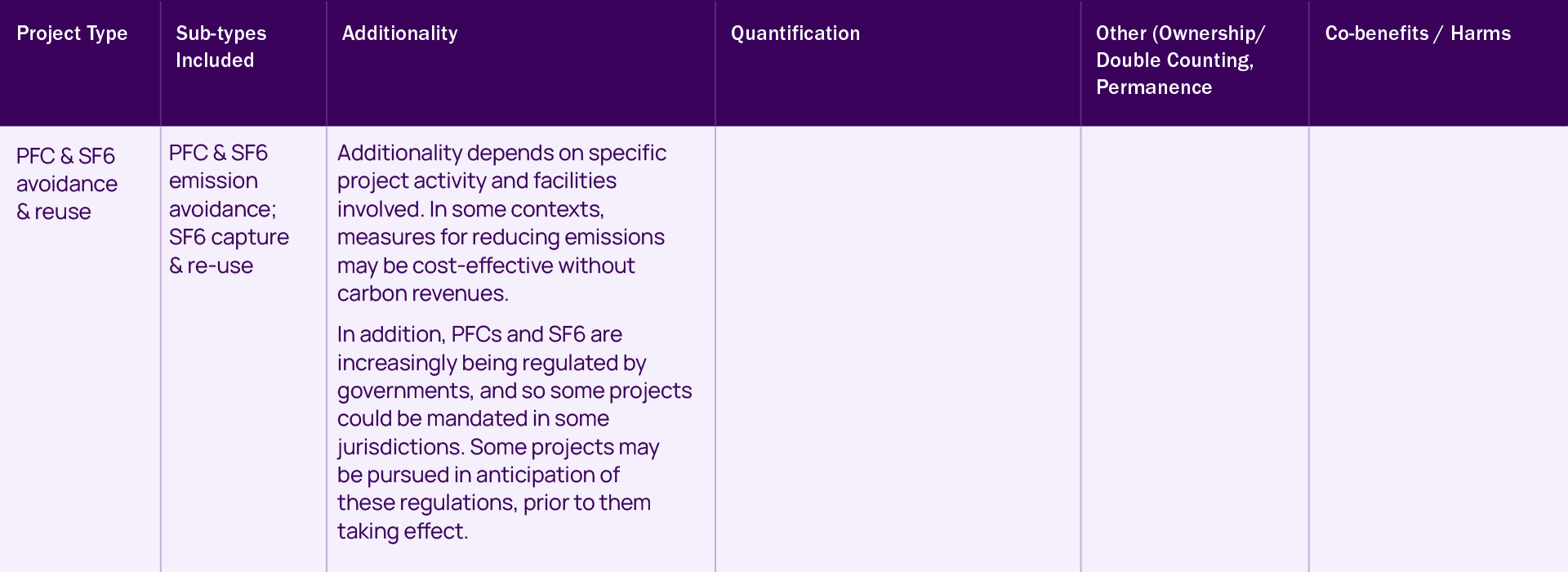

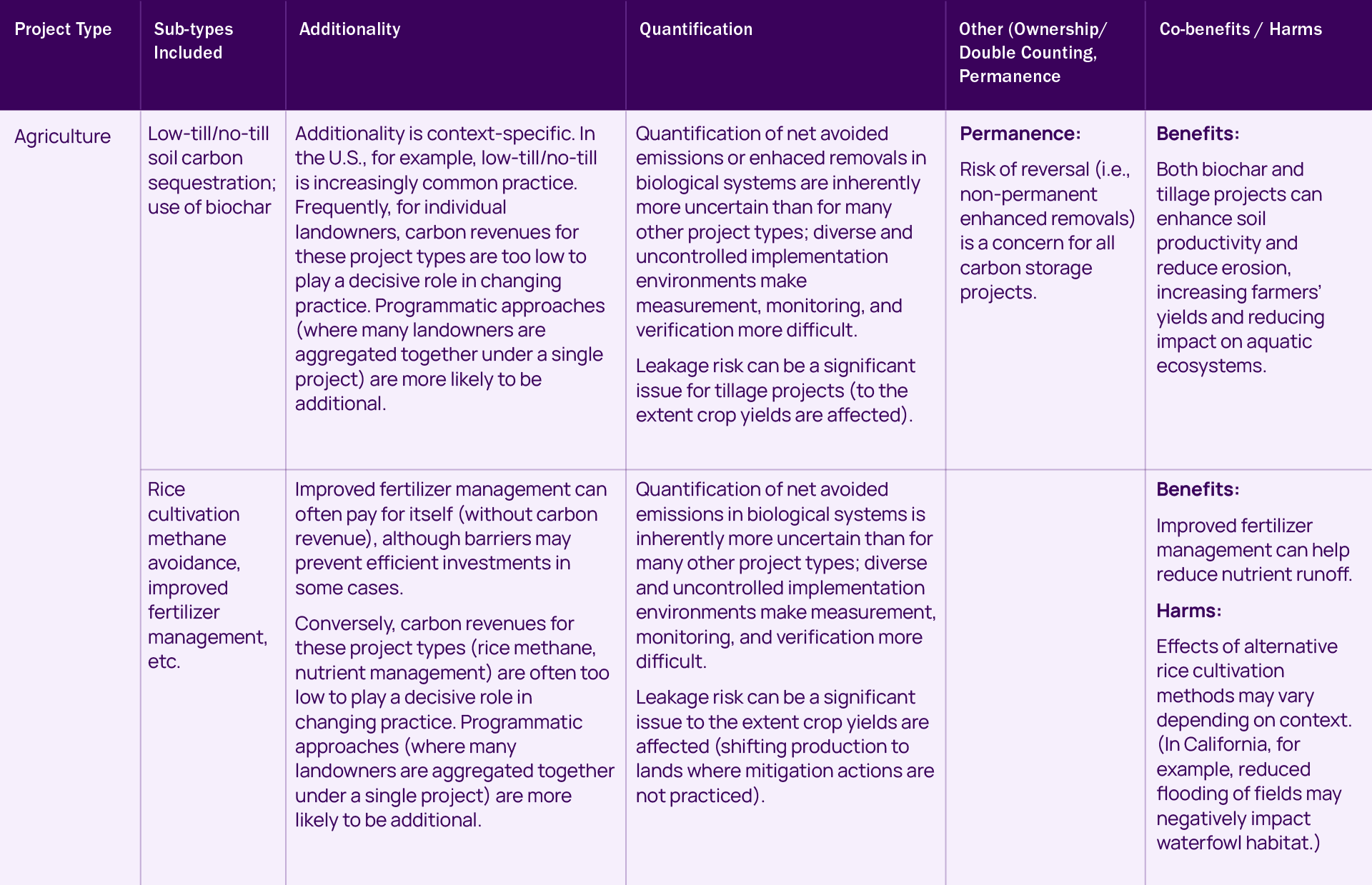

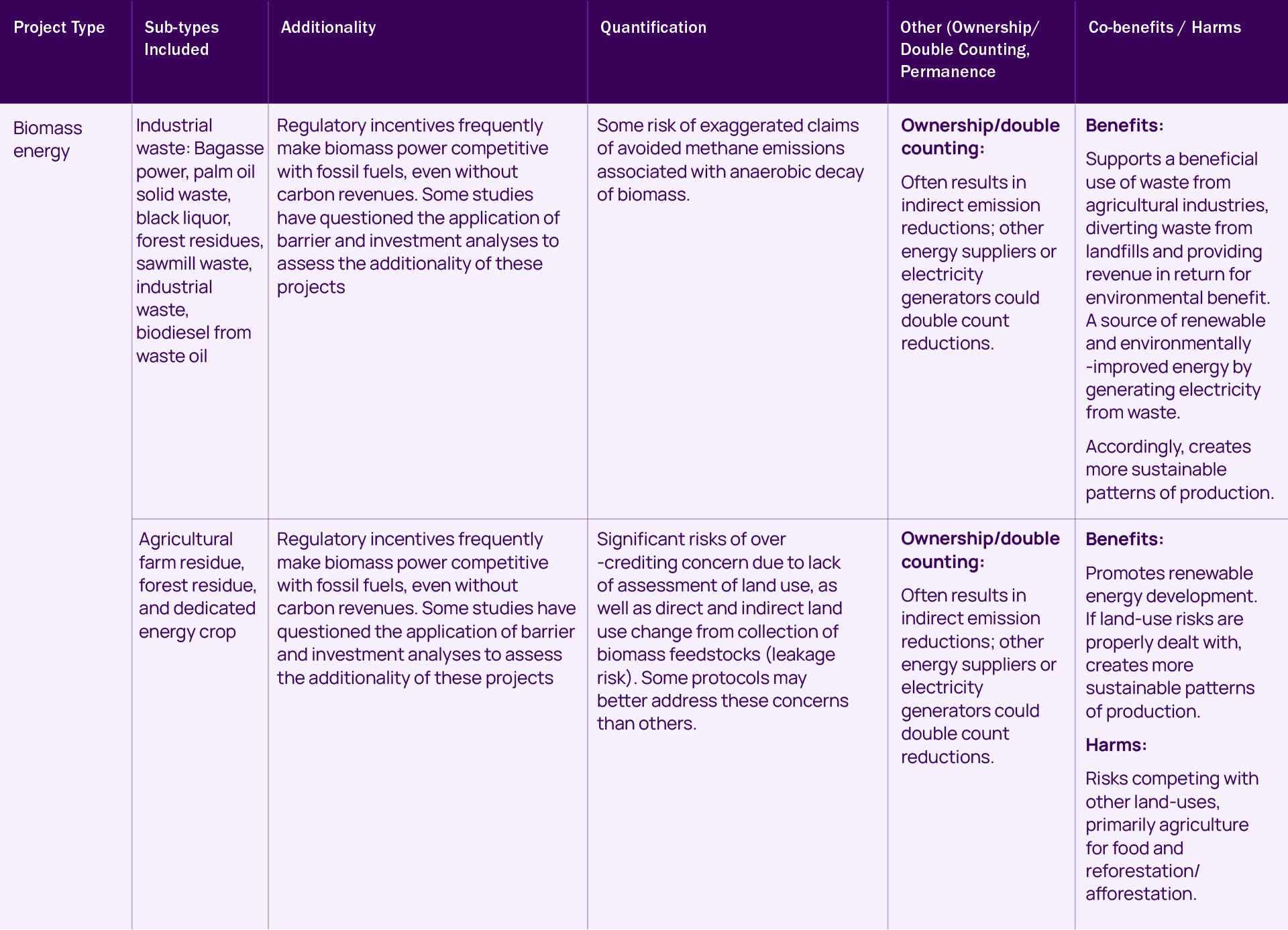

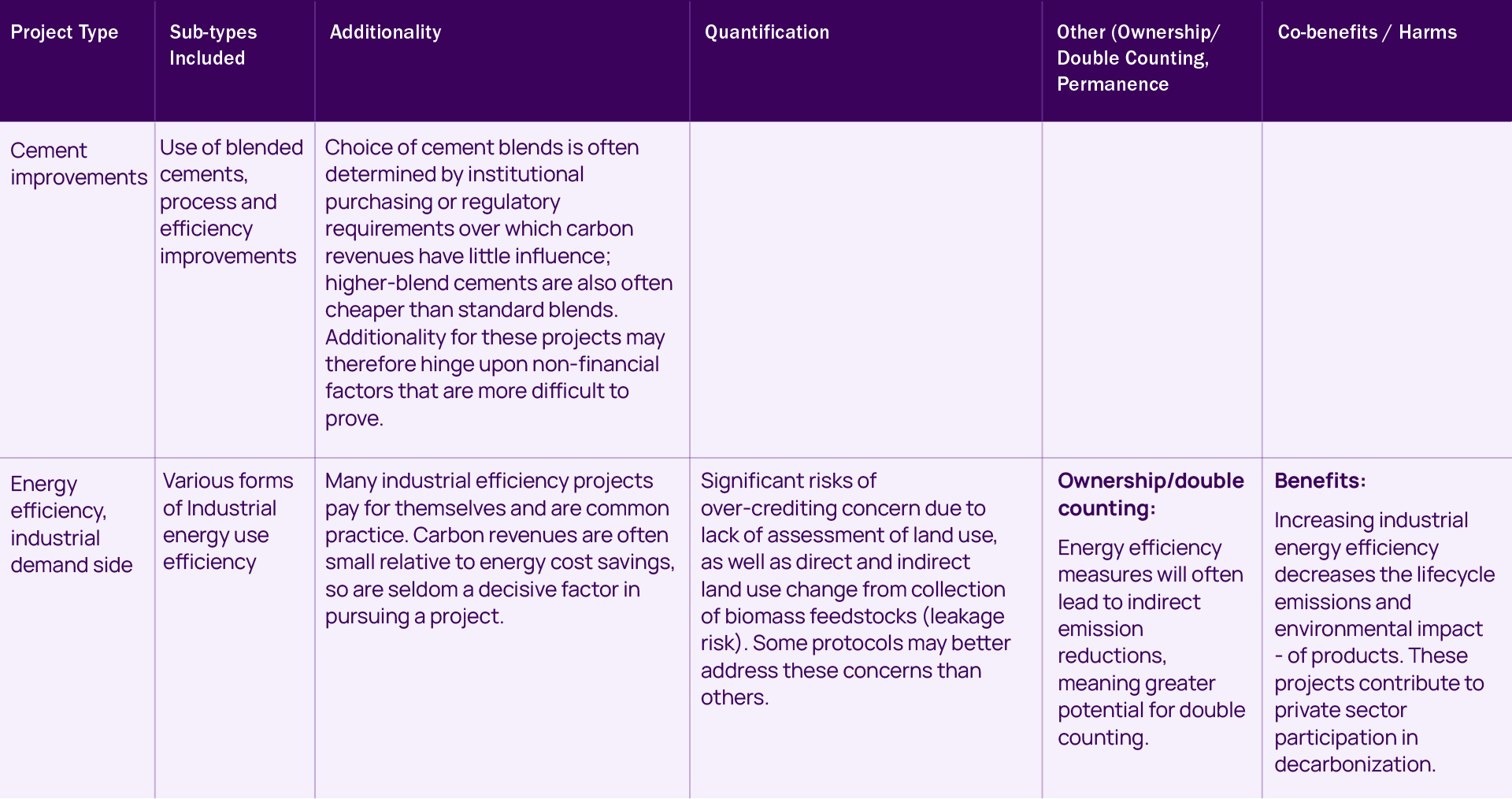

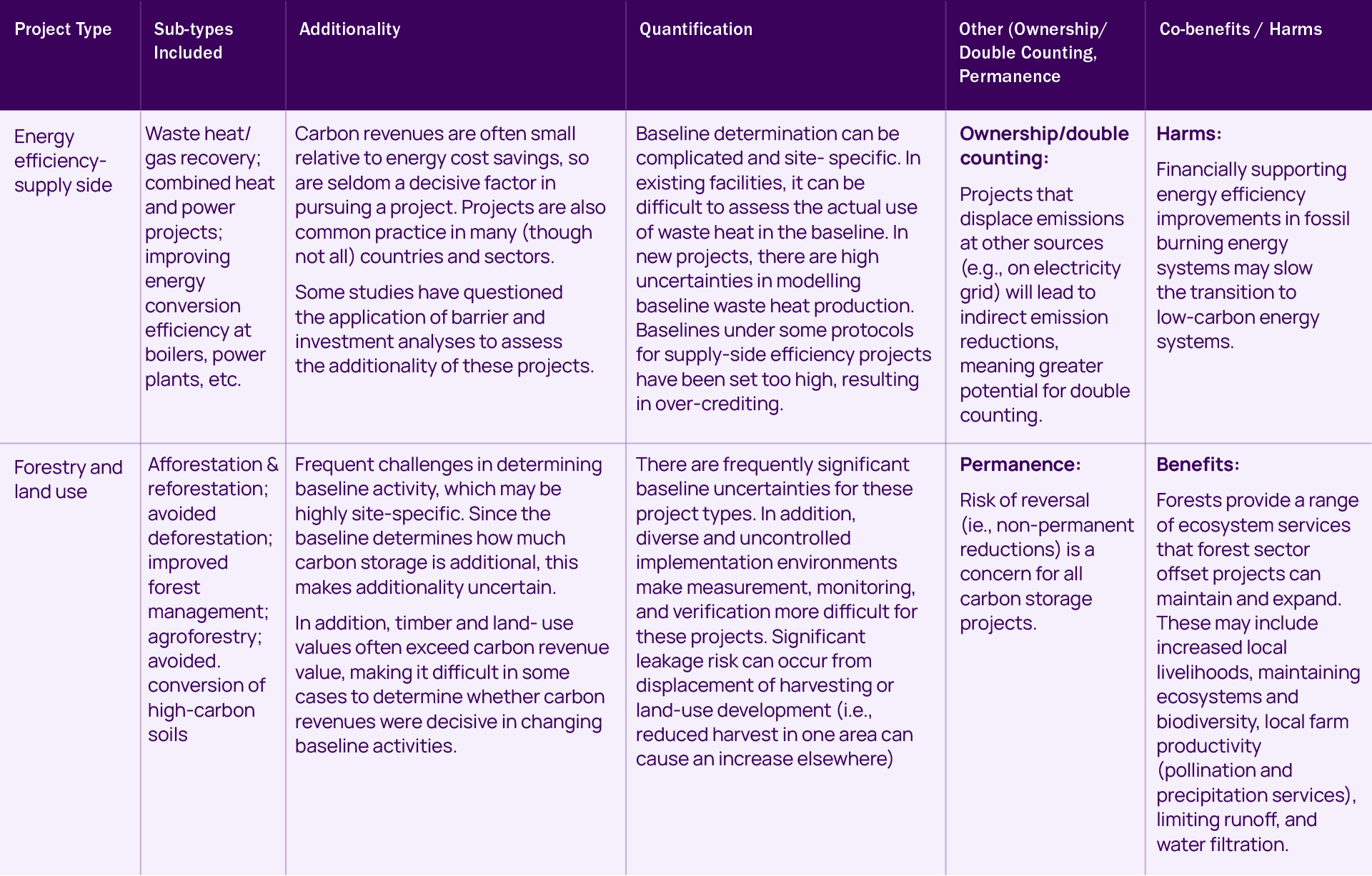

Overview of Lower, Medium, and Higher Risk tables presenting relative credit quality risk for different project types:| Lower-Risk Project Types | Medium-Risk Project Types | Higher-Risk Project Types |

| – Carbon dioxide (CO2) usage | – Methane (CH4) capture and utilization | – Agriculture |

| – Methane (CH4) destruction (w/o utilization) | – Methane (CH4) avoidance | – Biomass energy |

| – Nitrous oxide (N2O) avoidance from nitric acid production | – Energy distribution | – Energy efficiency, industrial demand side |

| – Nitrous oxide (N2O), adipic acid | – Energy efficiency, household demand side | – Energy efficiency, supply side |

| – Ozone-depleting substance (ODS) destruction | – Perfluorocarbons (PFC) and sulfur hexafluoride (SF6) avoidance/reuse | – Forestry and land use |

| – Direct air carbon capture and storage | – Renewable energy, small scale | – Fossil fuel switching |

| – Enhanced weathering | – Fugitive gas capture or avoidance | |

| – Low-carbon transportation measures | ||

| – Renewable energy, large scale |

Expand the sections below to see details on each project type

Lower-Risk Project Types

Medium-Risk Project Types

Higher-Risk Project Types

Download Annex 1 of the Carbon Offset Guide: Offset Project Types and Relative Quality Risks

Buying credits from trusted exchanges or retailers

As discussed in How To Acquire Carbon Credits, a common way to purchase carbon credits is through a retailer or an exchange. Many of these services exist primarily to facilitate transactions and provide market liquidity, without necessarily making any representations about the quality of credits transacted (e.g., beyond indicating their origin and the standards against which they were issued). However, many retailers – and some carbon credit exchanges – market themselves as only providing higher-quality credits. Procuring carbon credits from a trustworthy “higher-quality” retailer or exchange is one way to avoid lower-quality credits.

The main challenge with this approach is ascertaining how trustworthy the service is and what their methods are for selecting higher-quality credits. One way to do this is to inquire about which of the various approaches described by this guide they themselves follow. For example, are they simply acquiring carbon credits issued under independently recognized crediting programs (see What Are Carbon Crediting Programs) – which may not be a reliable guarantee of quality? Or are they only making credits available from specific projects that are rated highly by an independent rating service?

Pros: Sticking to a reliable retailer or exchange for acquiring carbon credits can be a relatively easy way to avoid lower-quality credits, provided the retailer or exchange does a good job themselves of selecting for higher-quality.

Cons: This approach still requires care to determine the relative trustworthiness of the retailer or exchange and to evaluate the criteria they use to select higher-quality carbon credits.

Buying credits from projects certified against independently assessed, higher-quality methodologies

A relatively recent development in the voluntary carbon market is the establishment of initiatives that independently assess both (1) crediting programs and their governance (like the initiatives described in buying credits issued by independently recognized crediting programs); and (2) the relative rigor and quality of individual methodologies used by these crediting programs to register projects and issue credits. These initiatives identify not just credible programs, but also which of the methodologies used by these programs tend to be higher-quality. Projects that follow more stringent methodologies, for example, stand a greater chance of clearing a high bar for quality.

Two prominent examples of these initiatives are the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Carbon Credit Quality Initiative (CCQI). The goal of the ICVCM is to identify specific project categories (crediting program and project type combinations) that meet a threshold for quality (or “integrity,” as defined by the ICVCM). The CCQI rates individual methodologies on a five-point scale, indicating how they compare both within and across crediting programs (which in some cases also considers differences in crediting program governance and procedures).

The International Civil Aviation Organization (ICAO) is also selective about the specific methodologies that are eligible for use under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). However, ICAO’s decisions to exclude methodologies are typically based on policy considerations, not an explicit assessment of their quality deficits. The primary hurdle for eligibility under CORSIA is meeting programmatic requirements and it is therefore not strictly comparable to the ICVCM or CCQI initiatives.

Examples

Established: 2021 (still under development)

The ICVCM was established as an independent governance body for the voluntary carbon market, initiated by carbon market stakeholders and leaders in climate finance. It has identified “Core Carbon Principles” (CCPs) that define quality thresholds for specific combinations of crediting programs and carbon credit methodologies. The ICVCM is in the process of assessing crediting programs’ approved methodologies against the CCPs, initially targeting the methodologies that comprise the largest share of credits in the voluntary market. The assessment will determine which methodologies meet the CCP quality thresholds and can therefore be labeled as higher-quality.

Established: 2021

The CCQI is an initiative founded and managed by three non-profit organizations: the Environmental Defense Fund (EDF), the World Wildlife Fund (WWF), and Oeko Institute. The CCQI evaluates crediting programs and individual methodologies and assigns quality rating scores specific to each methodology (see CCQI FAQ for more information). The CCQI has made its methodology publicly available online and publishes the results of scores which are integrated into an online scoring tool. The tool guides users to select the type of project they are interested in, the crediting program, the country of implementation, the timing of the avoided emissions or enhanced removals, and the specific methodology that was selected. Each of these factors can potentially result in different scores based upon the assessment CCQI experts have conducted.

Pros: These initiatives allow buyers to identify carbon credits issued under more rigorous standards and methodologies, thus reducing the risk that the credits will be of lower-quality. This may be a more reliable approach than, for example, sticking to lower risk project types, because even within a project category, the methodologies used by crediting programs can be more or less stringent. Moreover, higher-quality methodologies can help guard against poor-quality carbon credits even for project types with higher inherent risk, thus expanding the pool of potentially “safe” carbon credits.

Cons: Rating credits at the methodology (or program and methodology) level may still be a blunt way to discriminate between higher- and lower-quality credits. There is still a risk of “bad” (lower-quality) projects being certified under higher-quality methodologies. Conversely, it is often still possible to find higher-quality projects registered under lower-rated methodologies. Truly understanding the relative quality of carbon credits may require project-level reviews, which these initiatives do not provide.

Least reliable methods

A few “quick and easy” approaches can be used to provide at least some assurance of avoiding lower-quality or less credible carbon credits.

- Buying credits issued by independently recognized crediting programs

- Avoiding cheaper credits

- Avoiding older credit “vintages”

- Making up for low-quality by discounting or over buying

Buying credits issued by independently recognized crediting programs

Over the years, several independent organizations and initiatives have been established to evaluate and accredit carbon crediting programs. In some cases, these organizations were formed to provide greater assurance for voluntary buyers by assessing and recognizing crediting programs that meet defined standards for governance, oversight, and standards development. In other cases, regulatory bodies – like the International Civil Aviation Organization (ICAO) – have developed standards for recognizing crediting programs that are eligible to serve the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

Pros: These kinds of recognition programs help to distinguish crediting programs with credible standards and governance systems from those that may be less reliable. For example, they typically ensure that recognized crediting programs are free from conflicts of interest, e.g., they do not certify and then directly sell credits to buyers.

Cons: Even within established crediting programs, there can be significant variations in quality among different project types (and even between specific registered projects). Buying carbon credits from a recognized program helps to avoid serious credibility challenges, but is not a guarantee of buying higher-quality credits.

Examples:

Established: 2008

The International Carbon Reduction and Offset Alliance (ICROA) is an industry trade group established to promote best practices within the voluntary carbon market. Purchasing credits from ICROA-endorsed crediting programs can offer buyers the assurance that thresholds for program operations and management have been met. ICROA requirements include: demonstration of a program’s independence from conflict of interest, markets, and project developers; effective governance practices; the use of a registry tracking system; public availability of information and transparency of procedures; the use of third-party auditors to review individual projects as well as procedures for auditor oversight; the use of carbon crediting principles to inform standard requirements; the consideration of stakeholder views through the program’s development and operation; and a requirement that each program surpasses a scale threshold of listed projects (>2) and issued credits (>100,000tCO2e).

Established: 2008

Serving mainly North American buyers, the Green-e Climate program provides “independent oversight of marketing and sales, [so that] buyers can be sure they are getting what they paid for.” Green-e has endorsed four carbon crediting programs to date for which credits may be eligible for the Green-e Climate label including the Gold Standard, Verra’s Verified Carbon Standard (VCS), the Climate Action Reserve (CAR), and ACR. The Green-e label conveys chain-of-custody certification for the carbon credit – meaning that the credit’s chain of custody pathway from project implementation and credit issuance to the project developer via a registry system, through any transactions between intermediary credit brokers, traders, or exchanges, to the ultimate use and retirement of the credit in the registry tracking system has been recorded accurately and supports the exclusive claim of the credit by the buyer.

Established: 2016

The International Civil Aviation Organization (ICAO) proposed a goal to achieve carbon neutral growth in international aviation beyond 2020 in 2010. In 2016 it began development of a market-based mechanism – the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) – to realize this goal. The CORSIA program3 identifies existing carbon crediting programs from which airlines may source carbon credits to comply with carbon neutral growth requirements. However, in some cases CORSIA also further restricts eligibility of credits to those derived from approved project types or methodologies (see Buying credits from projects certified against independently assessed, higher-quality methodologies).

Avoiding cheaper credits

In many markets, “cheap” is often synonymous with “lower-quality.” Very cheap carbon credits can indeed be a sign of lower-quality, especially for newer projects. If a project is selling carbon credits for a price below US$1-2 per tonne (i.e., close to the transaction cost of getting a project developed, registered, and verified) then the case for additionality is probably weak; it can be hard to argue that the project truly depended on carbon credit revenue for its implementation. However, some carbon project types with high environmental integrity can avoid GHG emissions or enhance removals at relatively low cost (e.g., some types of industrial gas destruction).

The inverse argument – that higher prices correlate with higher quality – is not reliably true either. Truly additional crediting projects will have a higher intrinsic cost for avoided GHG emissions or enhanced removals and will therefore need to charge a higher price for carbon credits to be financially viable. However, there is nothing to prevent non-additional projects from also charging high prices, assuming they can find a gullible buyer. These projects may end up crowding out projects with higher actual costs.

Pros: Purchasing more expensive credits may mean a higher likelihood of additionality, as well as higher scores on other criteria like quantification, permanence, and avoidance of social and environmental harms.

Cons: Looking only for higher-priced carbon credits (without looking at other variables) is not a guarantee of higher quality.

Avoiding older credit “vintages”

The “vintage” of an carbon credit can refer either to the year in which it was issued, or the year in which its associated avoided GHG emissions or enhanced removals occurred (for some kinds of carbon credit projects, there can be a significant lag between the emissions impact and issuance, because of longer verification cycles, e.g., with forestry projects). Older issuance vintages may present a quality concern where the following conditions are true:

- The carbon credits under consideration have remained unsold for a long time; and/or

- The carbon credits are being sold directly by the project developer, where the developer:

- Did not contract with a dedicated carbon credit buyer upfront (e.g., under an emissions reductions payment agreement (ERPA)); and/or

- Has carried forward a significant number of unsold carbon credits; and

- Has continued to operate the carbon project for several years despite the lack of carbon credit sales.

Pros: Avoiding the purchase of older credit vintages can avoid cases where credits were obviously lower-quality to begin with. It may also help to ensure that the purchase is driving new efforts to avoid emissions or enhance removals. (Even if an old project was high-quality to begin with, if it is now complete or near completion, or it has succeeded for years without selling some credits, then buying unsold credits may not contribute to addressing climate change beyond merely supporting a “sunk” benefit of the project.)

Cons: The vintage of a carbon credit does not by itself indicate anything about its quality.

Making up for low-quality by discounting or over buying

One strategy to address quality risks is to simply retire extra carbon credits. For example, to compensate for 100 tonnes of CO2 emissions, a buyer could purchase and retire 200 carbon credits from a range of different projects. This approach is commonly referred to as “discounting.”4

Although this strategy does not address quality directly, it hedges against the risk that some carbon credits may be associated with avoided emissions or enhanced removals that are non-additional, overestimated, non-permanent, or claimed by others. It may also help buyers focus on reducing their own emissions, since it effectively increases the cost of offsetting.

Pros: Discounting or “over-buying” credits can help make up for deficits in quality across a portfolio of carbon credits and project types. It can be particularly useful where the recognized quality deficit relates to overestimation. For example, if the project was issued twice as many credits as it should have been, then purchasing and retiring two credits for every tonne of claimed mitigation could be an effective strategy.

Cons: While discounting can be part of a responsible strategy for using carbon credits, it should not be done in the absence of other methods to assess quality and avoid lower-quality credits. Doubling the purchase of non-additional credits still means that 100% of purchases are non-additional.

Due diligence sample case

This sample case presents answers to the due diligence questions for a sample case study of a fictional agricultural project.

Company X’s Sustainability Officer selected a project type from the Project Type Relative Quality Risk: Medium table: Agriculture and land use. The project type was appealing for its connection to Company X’s supply chain which relies upon agricultural products.

The Sustainability Officer, working with their offset broker, selected an improved fertilizer management project implemented in 2018 for further due diligence. The project developers claimed to be reducing N2O emissions (with a Global Warming Potential 298 times more powerful than CO2) through a reduction in synthetic nitrogen fertilizer applied to cropland. The project, a 2,000 acre corn farming operation, implemented a precision fertilizer application system in which increased soil analysis and new GPS integrated tractors allow farmers to avoid over-fertilization by applying fertilizer only where soil analysis indicates it is needed. The baseline scenario was stated to be the application of fertilizer uniformly across the entire field.

The Project Type Relative Quality Risk identifies Agriculture and land use as having issues requiring due diligence for both additionality and quantification. The Sustainability Officer downloaded the Project Design Document (PDD) from the publicly accessible registry, the project’s verification report from the timeframe in which the credits were generated, as well as the protocol applied to implement the project via the offset program’s website. They then began to answer the questions using the PDD, verification report, and protocol project information as sources to locate answers. Note that not all questions from the due diligence section are presented, as the Sustainability Officer engaged local experts familiar with the project and consulted colleagues in the offset professional community to narrow down the questions that would be most pertinent to the project and its unique context.

Additionality: The project claims to be additional based upon a minimal rate of technology adoption within similar large-scale corn farms, upfront financial investment barriers to purchase new (more expensive) tractors and perform more detailed soil analysis, that were overcome by carbon offset financing.

- Are data and assumptions used to justify the project’s additionality available and easily accessible? AND How much information and data has the project provided to establish its claim to additionality? AND Is there a compelling argument that the project activity is not common practice?

The PDD references a study from the previous year that analyzed the technology adoption rate amongst large-scale corn farms nationally. The study is from a reputable peer reviewed journal and identifies an adoption rate of <5% of 250 surveyed similarly sized (large-scale) corn farming operations in the US. The PDD also includes financial analysis (ROI calculation) outlining the cost of implementing increased soil analysis and tractor improvements and the anticipated cost-savings from reduced nitrogen fertilizer applied to fields.

- How large is the project’s offset credit revenue stream compared to other revenue streams or cost savings achieved by the project? AND Is there a clear and believable case that offset credit revenues were a decisive factor in pursuing the project?

The project’s offset credit revenue stream appears to be a small proportion (~15%) of total revenue generated by the project, yet the financial analysis was presented as the primary decision making tool for whether to implement the project. The project requires a large upfront investment of improved tractor technology and results in annual cost savings from reduced nitrogen fertilizer application. The cost savings of implementing the project, factored into the financial analysis and helped the project move forward with the investment – which was flagged for further follow-up because of the potential additionality concern. Upon closer examination of the project documents, despite the offset revenue being a small portion of the overall project revenue (and cost savings), the PDD made an effective case for this additional 15% revenue which tipped the scales during the financial analysis phase of project development. The addition of carbon revenue reduced the payback period from 10 to 7 years and thereby made the improvements economically viable for the farmer.

- Would the project cease reducing emissions if it did not continue to receive carbon offset revenues?

After the project was implemented, it would likely not cease reducing emissions without the carbon offset revenue due to the large upfront investment in new tractor technology that is a ‘sunk cost,’ as well as the ongoing cost savings from reduced nitrogen fertilizer consumption. The project is limited by its offset crediting period of 10 years. However, if the project were to pursue a second 10-year crediting period, then its additionality would be highly suspect given that the ROI timeframe of the financial investment analysis will have elapsed.

Quantification: The protocol’s methodology calculates GHG reductions through estimation of the amount of fertilizer reduced from the baseline scenario and utilizes the protocol-recommended peer-reviewed quantification tool. Quantification of project impact was completed through project verification (if accessible the verification report may provide useful information to answer the following questions).

- Is the quantification protocol methodologically and scientifically sound?

An internet and literature search of the protocol’s quantification methodology finds numerous references citing uncertainty regarding the rate of release of N2O from applying synthetic nitrogen fertilizer to cropland. The quantification methodology assesses the expected release of N2O in the baseline scenario and the actual release of N2O from applied fertilizer in the project scenario using the same method and conservatively underestimates the reduction – by reducing the impact claimed from measured fertilizer reductions by 10% to account for unforeseen circumstances – which decreases the risk of over-crediting. The literature is well established demonstrating that reduction in the amount of nitrogen fertilizer applied will reduce GHG emissions and that tracking the reductions of fertilizer applied can produce accurate measurements, to within +/-5% of overall climate impact. By applying a 10% reduction of impact, the quantification methodology uses a conservative approach to estimating impact in recognition of the inherent quantification uncertainties.

- Are protocol-prescribed methods for addressing quantification uncertainties – including leakage risks – appropriate for the specific project being examined?

See the above answer regarding quantification methodology uncertainties. The protocol requires tracking additional agricultural equipment usage by the project and associated additional fuel and electricity required. These associated additional emissions calculated in the PDD, however, were deemed to be ‘de minimis’ sources (i.e., negligibly small).

One possible concern for this project type is that reduced fertilizer use will reduce the crop yield, and given the responsiveness of the corn market, reduced production on one farm is generally thought to increase production (i.e., use of fertilizer) on other farm sites – thereby negating the effect of the project (learn more about leakage). To account for this possible ‘market leakage’, the protocol requires that the project’s corn-yield data be compared against a baseline period to identify the site’s average yield. If yield was reduced following the fertilizer reduction regimen, the protocol provides appropriate recourse for adjusting the amount of fertilizer actually reduced by the project – to reflect the market leakage impact. The verification report for this project indicates that the precision fertilizer application change did not reduce the farm’s corn yield.

- Joppa, L., Luers, A., Willmott, E., Friedmann, S. J., Hamburg, S. P. and Broze, R. (2021). Microsoft’s million-tonne CO2-removal purchase — lessons for net zero. Nature, 597(7878). 629–32. DOI:10.1038/d41586-021-02606-3. ↩︎

- While additionality is not usually a concern, it may be in some cases (e.g., where most industry players, or a particular actor, have already agreed to voluntarily mitigate emissions). Furthermore, some kinds of industrial gas projects have issues with baseline estimation and overestimation of avoided emissions. ↩︎

- For more information regarding how the CORSIA program functions see this report. ↩︎

- Technically, “discounting” refers to issuing fewer credits to a project than the avoided emissions or enhanced removals it achieved, but it is often used more broadly to refer to any approach that effectively uses more than a 1:1 ratio of carbon credits to compensate for tCO2e emissions. It has also been proposed as an approach for use in regulatory carbon markets; for example, see Warnecke et al. (2014). ↩︎

offsetguide